US reaction: Core inflation sticky again, but eclipsed by jobless claims

- 10 October 2024 (5 min read)

KEY POINTS

US CPI inflation came in above consensus for September, the headline rate easing to 2.4% from 2.5% in August, but firmer than the expected 2.3% (a 0.2% monthly gain compared to a 0.1% expected). Core inflation reported its second consecutive above consensus report, rising on the month by 0.3% - the same as last month (0.31% vs 0.28% unrounded) – compared to expectations for 0.2%. The core annual rate of inflation edged higher to 3.3%, back to its June level – although still a 3-year low before that.

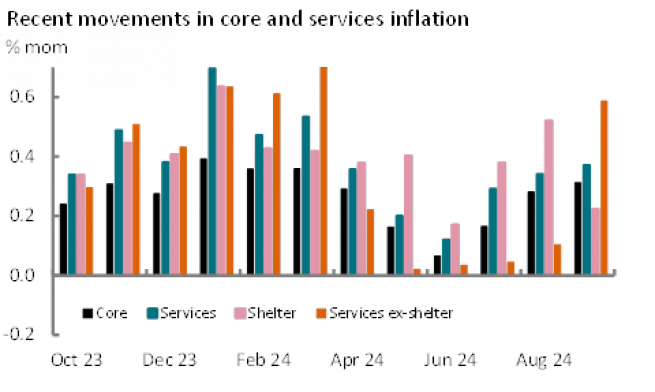

Although the CPI miss to consensus was small in overall terms, albeit the second such for ‘core’, the details of the report add a little more caution. First, today’s inflation reading came despite a very benign month for oil prices, feeding through to gasoline prices. Gasoline fell by 4% on the month (adjusted) compared with a modest rise last year. This took 0.2% off the headline rate in September. Importantly this looks likely to unwind next month with oil prices having picked up across October, versus a sharp 4.3% drop last October. Second, the more modest impact from services inflation, which rose by 0.4% on the month and took the annual rate to 4.7% and a 32-month low, was buoyed by the weakening in shelter inflation, which gained just 0.2% on the month. This is the second weakest monthly print in 3-years and adds further evidence that an eventual slowdown in housing costs is starting to materialize (after an unusually firm 0.5% rise last month). However, from the Fed’s point of view, Fed Chair Powell had made it clear that the Fed was pretty much assuming that this was in the post, whether in the data or not. Third, what a modest services versus weak shelter inflation print means is that ex-shelter inflation spiked. This measure rose by 0.6% - in line with two of the three months at the start of the year that caused the Fed to delay the commencement of its easing cycle – in turn driven by solid gains in education and medical care costs.

In broad terms, the case for US disinflation is broadly unchanged. Headline inflation is at a 3½ year low; core still close to a three year low. This suggests space for the Fed to continue to ease the restrictiveness of policy. However, we suggest that depressed energy prices are contributing to the weakness in headline inflation – and may not persist - with core inflation still elevated by shelter inflation (4.9% y/y), which should ease, but with ex-shelter services inflation also high at 4.4%, which may not. The question then is about how quickly the Fed may ease policy. The minutes to September’s FOMC meeting stated that a ”substantial majority” supported the 50bps move. But the minutes also reported that “some” would have “preferred a 25bps reduction”, while “a few .. could have supported such a decision” and “Several .. that [25bps] would be in line with a gradual path of policy normalization”. This conveys a sense of meaningful pushback from the Committee in September. Today’s figures remind that there is likely to be some need for restrictive policy over the coming quarters to ensure that inflation returns to target on a sustained basis. With financial conditions now looser than the average of the previous decade, we argue that the Fed’s implicit endorsement of the market’s aggressive expected easing is overcooked. Indeed, following the recent payrolls print markets have repriced the outlook for Fed easing. We forecast two 25bps cuts over the next two meetings. However, we suggest that market and Fed expectations that rate cuts will continue smoothly across next year will be election dependent. We see several election scenarios, including the re-election of former President Trump, where the Fed’s space to ease policy is restricted across the course of next year.

Market reaction, however, was dominated by the sharp jump in jobless claims, which rose by 33k to 258k – the most in more than a year. Much of this we believe to reflect disruption from hurricane Helene, but the report also identified a rise in Michigan lay-offs, which is likely in part reflecting reduced shifts at Stellantis. Jobless claims could be elevated for a number of weeks reflecting ongoing hurricane disruption and this is likely to keep the market and Fed cautious. Markets halved the previous probability of the Fed not cutting in November, now seeing just a 16% chance of no move, and increased the likelihood of two 0.25% cuts this year to 80%. 2-year US Treasury yields dropped 6bps to 3.98% and 10-year fell by 2bps to 4.07% - although still the highest levels since end-July. The dollar dropped 0.2% against a basket of currencies, but also remains at its firmest since early August.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved