European High Yield - Outlook 2025 Out with the old, in with the... same?

- 09 December 2024 (7 min read)

KEY POINTS

This time last year, we wrote about how our - and most people’s - base case was for a so-called ‘soft-landing,’ of lower interest rates and, at worst, a mild recession in developed economies. We then projected the positive environment for European high yield that seems to have been realised: helped by tighter spreads, returns are indeed set to be a reasonable margin even above the starting yield of 6.6% (they were +8.0% through the end of November 2024). This is broadly in-line with US high yield (+8.7%), compares favourably with European investment grade (+5.1%) and is only a short way behind the EuroStoxx 600 (+10.1%).1

What we hadn’t anticipated was, rolling forwards 12 months, the policy uncertainties which existed at the end of 2023 would largely still be in place in December 2024. We thought that by now, it would be possible to rule out either a deeper recession or persistently elevated levels of inflation – respectively, the ‘hard landing’ and ‘no landing’ tail-risks which we flagged a year ago. And at the end of Q3, this was basically the case. The Federal Reserve (‘Fed’) had just cut rates by 50 basis points (‘bps’) at its September meeting; investors were pricing almost continual reductions until the middle of next year; and the ability of the monthly inflation figures to roil markets seemed to have, at least in this cycle, firmly passed. But in a year of geopolitical shocks, Donald Trump’s convincing victory in the US election still took markets by surprise. With an economic agenda based on tariffs and tax cuts, more inflation and higher rates are therefore firmly back on the table. And whilst the policy picture in Europe appears rather different, the ability of the Fed to influence interest rates worldwide should not be underestimated.

The above serves as a rather long way of saying that, as was the case for 2024, we see three possible paths for our asset class in 2025:

- Still favoured by the market, our central forecast is again that a soft-landing occurs. But with spreads and front-end interest rates having less room to rally further, carry will dominate returns for European high yield. We would expect these to be of the order of the starting level of yield, currently +5.9%.

- Now firmly back on the agenda… a Fed which has less room for easing, and interest rates which stay higher. High yield should of course be somewhat protected by its naturally shorter duration and healthy levels of income. Though some of the challenges to fundamentals that this would represent would inevitably have to be reflected in wider spreads. We project gains a little lower than in the first scenario.

- There is still a chance that central banks are behind the curve and developed economies tip into a more severe recession. Spreads would clearly have to widen even more in such an instance, impacting returns. But as detailed below, we do not think all would be doom-and-gloom in our market.

Though valuations in European high yield appear less compelling than they were 12 months ago, viewed through the lens of the possible outcomes above we think the balance of risk and reward remains very attractive. And ultimately, the events of early November actually give us even more conviction that 2025 will be a year for defensive carry as we wait to see how this cycle ends.

Carry? What carry?

It’s true – European high yield spreads are around 50bps tighter than they were in January.

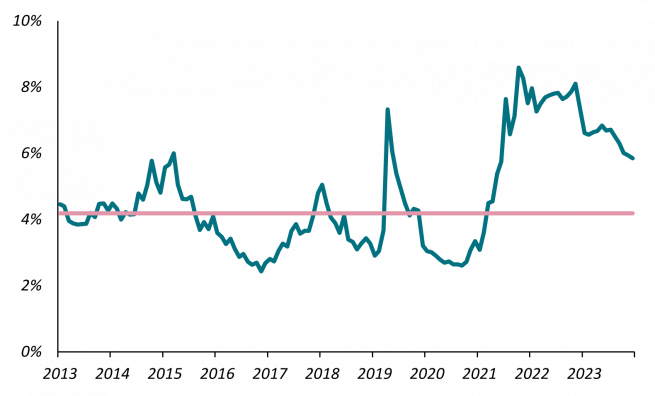

Still, it is undeniable that all-in-yields remain elevated. They are quite clearly still near the peaks of the last decade or so, and well above the median from that period:

- U291cmNlOiBCbG9vbWJlcmcsIGFzIG9mIDMwIE5vdmVtYmVyIDIwMjQu

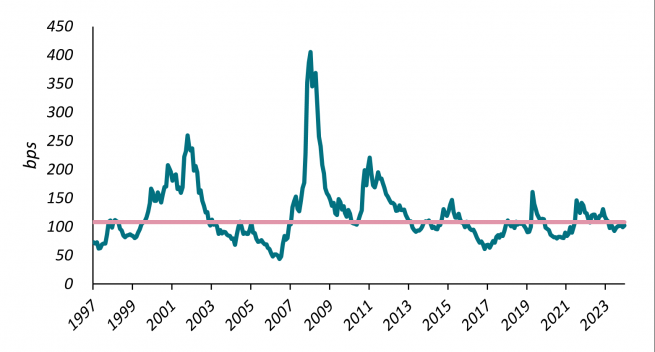

And actually, even just looking at spreads, when we adjust these to account for the shorter duration of the universe, they also appear only slightly inside the very long-term median.

Not-so-speculative grade

Speaking of risks, talk of ‘defensive’ carry in high yield is less of a contradiction than it appears. We can show this in a few different ways.

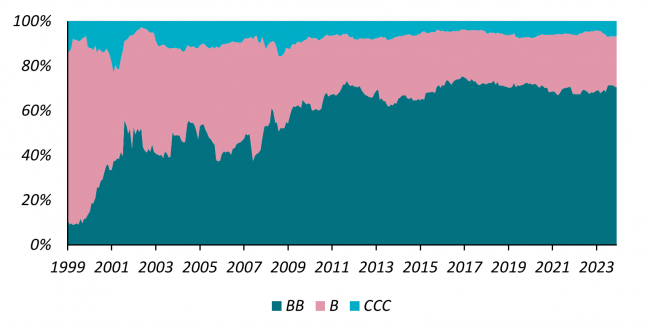

In terms of ratings, the European high yield market skews heavily towards BBs – the strongest part of the spectrum. The proportion has been around 70% since 2016, currently sitting exactly at that level. This marks an interesting point of comparison with US high yield where BBs have only rarely represented more than a majority of the universe.

Whilst ratings can only ever be a backwards-looking proxy for credit quality, it is demonstrably true that the historical default experience of companies rated BB is very benign (the below numbers are for US high yield, since the data is more readily available - but the European figures would be similar). Even during the Global Financial Crisis in 2009, BB defaults never rose above 2.8%.

Even in a milder downside scenario, spread widening is almost always less severe for bonds in this cohort.

Alternatively, consider issue size. Whilst a somewhat crude proxy for liquidity and credit quality, the gradual increase in the average size of a single bond in our market suggests that it has grown both more liquid, and populated by bigger companies. From an average issue size of only €100m at inception in 1997, that stands at almost €550m today2 .

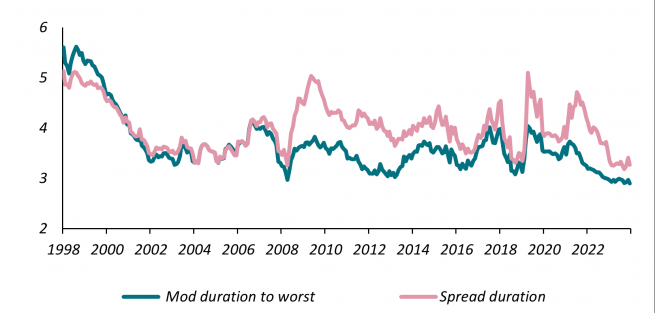

Finally, we have duration:

- U291cmNlOiBCbG9vbWJlcmcgYXMgb2YgMzAgTm92ZW1iZXIgMjAyNC4=

The very low volume of primary issuance in 2022 and 2023 means that, both on a modified and spread duration basis, the European high yield market is still at historically low levels (and, incidentally, around 0.5 years less than the US - in-line with the long-term average). As well as a reduced sensitivity to both rates and spreads, at the individual credit level a shorter duration results, we believe, in a more fundamental defensive skew. Investors’ capital isn’t at risk for as long and, with a shorter time until the issuer needs to return to market to refinance its debt, management teams are incentivised to treat creditors well – so fewer dividends, and more debt paydown.

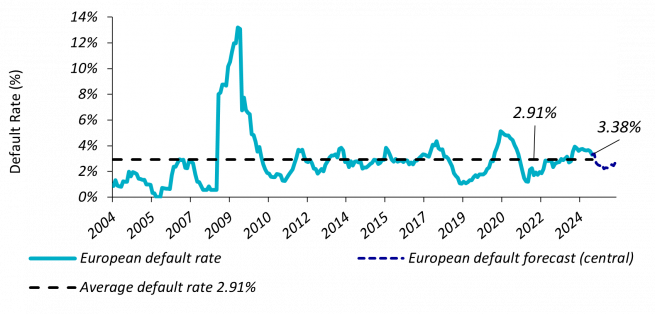

Not your usual default rate cycle, either

At a headline level, default rates have risen over the last year - a result of the record tightening in monetary conditions which has taken place since early-2022. But there are two mitigants to this trend. Firstly, the above chart includes distressed exchanges, which we’ve recently seen quite a few of. In these events, bonds are usually swapped for new, longer paper. This takes place at a price below par but, crucially, at a significantly higher level than a typical default recovery.

The other reason for comfort is that we forecast default rates to return to their long-term average level. Unsurprisingly, much of the reason for this rests with the ability of credits to successfully refinance – something which will become easier as the gap between current coupons and prevailing yields continues to close.

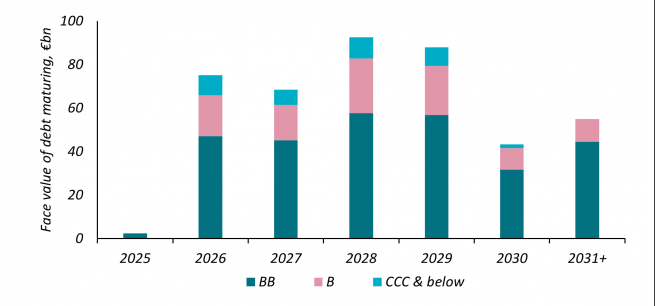

More money, fewer problems

The other two legs of support which we still believe are intact for our asset class are the technicals and the fundamentals. A year ago, we flagged that some investors had grown nervous about the ‘maturity wall’ – that is, the high volume of bonds which needed to be refinanced in 2024, ahead of looming 2025 maturities. Whilst we felt such fears were overblown, even we did not expect primary markets to rebound quite as they have this year. Up to the end of Q3, we are only slightly lagging the bumper 2021 calendar year in terms of gross new issuance. As a result, the maturity wall was easily dealt with. The picture now looks similarly manageable:

One corollary to primary markets that are open to refinancings is that net supply has slowly begun to increase, having been virtually non-existent in 2022 and 2023. This presents something of a challenge to the extremely strong technical that was in place a year ago. Then, a rapidly shrinking high yield market (over 25% of the face value of the ICE BofA European Currency High Yield Index was lost between the peak in mid-2021 and the low in April 2024) meant that spreads were squeezed tighter as investors chased fewer bonds. Now, as more credits have begun to test the waters with M&A deals, or dividend recapitalisations, we’re beginning to see the market grow again - a possible threat to that technical strength and, taken to extremes, a sign that ‘top of the market’ irrational exuberance is beginning to build up.

Still, we are a long way from that as yet. Though the M&A pipeline has likely bottomed, the economic environment is still not particularly conducive to a bumper number of deals. As has been the case for much of the last decade, the loan market is likely to absorb the vast majority of debt refinancing for LBOs. Overall, the current balance between a market that is open for business, yet still only seeing a slow pickup in new volumes, keeps us in a very supportive, favourable range.

Fundamentals are also trending positively. Despite headwinds in specific sectors (chemicals in the first half of the year, for example), and longstanding market concerns about a general consumer slowdown, we still see very little to make us nervous at a broad level. And as bottom-up, fundamental driven investors, we spend a lot of time talking to companies and studying trends in their businesses – they generally give us very few worries at this micro-level either.

Keep calm and carry on (defensively)

All of which leads us to the conclusion that there are currently few reasons for apprehension in European high yield. Even the most problematic sector of Q3 – autos – has not had a great impact on our market in general. The small number of single-B suppliers look challenged, but the vast bulk of names – BB companies like Renault, Volvo and Schaeffler – have so far seen just a small widening of spreads and bonds fall only a couple of points in price.

That’s not to deny that spreads have limited room to rally further – we think they are currently at about fair value. And of course, ours is an asset class that can underperform in an extreme downside scenario (or if uncertainties begin to emerge either here or from across the Atlantic...). But if 2025 is to be a year of watching and waiting political developments in this next phase of this cycle – and especially if the economy continues to run at neither too hot nor too cold – we think European high yield looks just right.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2024 AXA Investment Managers. All rights reserved

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.