Six things you need to know about the clean hydrogen economy - and why Europe is committed to it

Brussels has launched an ambitious plan for energy system integration with hydrogen and renewable sources, to help Europe become carbon free by 2050. Here is what should happen over the next 30 years.

What novelist Jules Verne wrote back in 1874 was confirmed by economist Jeremy Rifkin over a century later in 2002 - namely that hydrogen will play a fundamental role in the transition to clean and sustainable energy. The European Union (EU) Commission believes this strongly and plans to make significant financial investments in its ambitious European hydrogen strategy1, launched last July. Among other things, the plan provides for the installation of at least six gigawatts of electrolysers and the production of a million tons of clean hydrogen by 2024, set to increase to at least 40 gigawatts and 10 million tons respectively by 2030. But why is hydrogen important, how is the European strategy structured and what needs to change over the coming years?

European energy system integration

Europe’s target to become climate-neutral by 2050 imposes a need to transform the energy system, which accounts for 75% of greenhouse gas emissions. The key word here is ‘integration’. The current EU model consists of separate compartments - transport, industry and construction for instance - and represents its own story with different standards, value chains and operations. It is therefore essential to design and manage the entire European system as a whole, connecting infrastructure, production and consumption in a universal manner.

It is certainly no coincidence that Brussels launched its hydrogen strategy at the same time as the crucial Energy System Integration strategy.2 A flexible and interconnected network will be capable of combating climate change, as well as dramatically reducing costs for citizens and businesses. To give a few examples - our houses can be heated using heat generated by industrial plants, while energy from the solar panels on our roofs can recharge electric cars and factories can be powered by green energy produced by offshore wind farms. The list goes on.

The advantages of hydrogen: Zero emissions

Let’s look at why hydrogen is so important. There are three main reasons: First, it is a valuable ally in the fight against climate change as it produces zero emissions at end use - particularly in the transport, chemical, and iron and steel industries - but primarily because it can be produced via decarbonised processes (this is known as ‘green’ hydrogen) or methods with limited emissions (‘blue’ hydrogen, for which the CO2 is separated, captured, and then stored). More specifically, green hydrogen can be generated via electrolysis from renewable sources and blue hydrogen from a fossil fuel refining process, natural gas in particular. Indeed, hydrogen does not exist in its free state in nature but has to be extracted from other components that contain it.

- https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf

- https://ec.europa.eu/commission/presscorner/detail/en/ip_20_1259

Storage and integration with renewables

The second advantage of hydrogen is that it can be stored, in such a way that it compensates for the variability in flows of renewable, which depend on non-programmable meteorological factors such as the sun or wind. Solar, wind or hydroelectric energy can, in other words, be converted into hydrogen and stored in enormous tanks.

Ease of transportation

The third major advantage is that hydrogen can be transported easily via the existing natural gas distribution network: This means that it is not only possible to connect the production areas with the consumption areas, therefore supply and demand, but it also lowers the cost of supply (thereby ensuring security of supply).

The price component

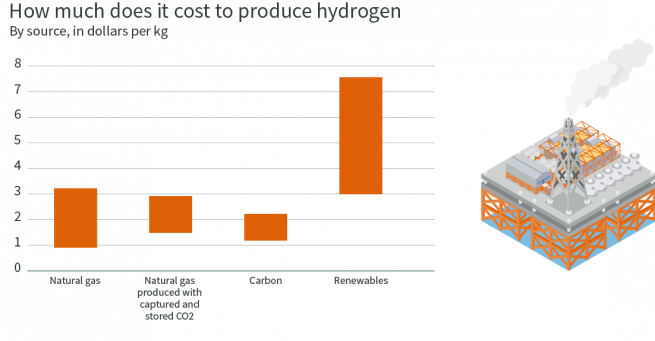

However, approximately 75% of hydrogen is ‘grey’, or produced using fossil fuels with significant CO2 emissions - approximately 830 million tons per year according to the International Energy Agency (IEA). This is because the production costs of ‘blue’ and ‘green’ variants remain high, despite the fact that technological innovation combined with the rise of renewables is set to lead to more competitive pricing in a few years. The IEA estimates that the cost of the hydrogen generated by renewables will fall by 30% by 2030.

The challenge of energy transformation

The hydrogen economy is colossal. According to Brussels, in Europe alone, the cumulative investments in the sector in 2050 could range from €180bn to €470bn.3 But for now, the development of the ‘green’ variant is only in its early stages. In the short and medium term ‘blue’ hydrogen will also be used, in order to support the creation of a profitable market. The EU Commission wishes to act at different levels with regard to energy transformation.

There are provisions for an infrastructure plan and strong financial support (as well as technological innovation), in addition to a review of legislation, fiscal aid, market governance reform and a gradual elimination of fossil fuel subsidies. Another crucial element is the establishment of major strategic partnerships that are being formed in several European countries.

This is the case in Norway, where a joint venture between Sunfire, Climeworks, Paul Wurth and Valinor is constructing the first plant for zero-emission aviation fuel produced from renewables. And in Denmark, key companies in the transport and energy sectors (including global shipping leader Maersk) have joined forces to create a large-scale plant for the production of green fuels.

But there is much work still to be done if hydrogen is to be the fuel of the future - which could create exciting potential new opportunities for investors.

- https://ec.europa.eu/energy/sites/ener/files/hydrogen_strategy.pdf

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.