Why US high yield continues to surprise investors

- 16 July 2024 (5 min read)

In 2023, many investors expected that the Federal Reserve’s (Fed) aggressive monetary policy tightening would lead to a potential recession and a pick-up in defaults in the high yield market. Given this backdrop, the broad market consensus was for investment grade to outperform high yield and, within high yield, higher quality BBs to outperform lower quality CCCs.

This consensus was wrong. Despite continued volatility in the US treasury market, the high yield market has benefited from a healthy fundamental backdrop and resilient US economy. Against this backdrop, US high yield companies have, despite diverging trends across sectors and issuers, performed better than anticipated.

Technical factors have also remained very supportive and, over the last couple of years, the market has seen a wave of rising stars to investment grade. This has surpassed the number of fallen angels. Alongside this, there has been less new issuance in the primary market, creating high demand for new deals when they do come to market.

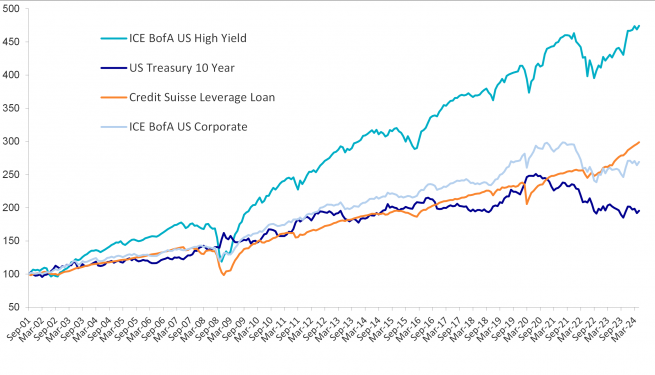

Looking across the high yield market, lower rated credit has outperformed higher quality in 2023 and 2024 year-to-date1 while shorter duration continues to outperform longer duration asset classes due to the inverted yield curve and continued rates volatility.

The US high yield market has outperformed investment grade, government bonds and cash over this time frame.

- IFNvdXJjZTogQVhBIElNLCBCbG9vbWJlcmcgYXMgb2YgMjV0aCBKdW5lIDIwMjQ=

Is there still room to run from here?

Looking at previous cycles, the high yield market tends to bounce back strongly after a sell-off. This is because as bond prices recover and coupons reset at higher levels, the level of income that bondholders receive increases. This is reflected in the all-in yield, which in the US high yield market moved from around 4% in 2021 to 9% at the start of 2023 and is now around 8%.2

This most recent sell-off, however was unusual compared to previous ones. 2022’s sell-off and rise in yields was driven mainly by interest rate increases, not by credit spreads widening. This means that bond prices today remain discounted as the outlook for interest rates has been uncertain. That could now be all about to change as we expect the Fed to start moderately easing policy in the second half of 2024.

This means that there is still significant upside potential for the high yield market through a combination of higher income and continued bond price recovery. It is worth bearing in mind that rallies in high yield can happen very quickly: in the fourth quarter of 2023, the US high yield market delivered a 7% total return as the market priced in rate cuts, with the average high yield market dollar price increasing from $88 in September to $93 by year-end, where it currently remains.3 Timing such market moves can be challenging so, we believe, being invested is important to ensure participation in rallies, whilst also benefitting from the higher carry now on offer.

We expect high yield spreads to continue to be supported by broadly healthy corporate fundamentals. We also expect any potential spread widening to be met with buyers, providing further technical support.

That said, dispersion is increasing as high yield companies adjust to a higher rate environment. This is reflected in how little of the US High Yield index is trading at its average YTW level. As of 12th June 2024, ~70% of the index had a YTW between 0 and 7.5% and ~20% had a YTW greater than 8.5%, leaving just ~10% of the overall market with a YTW between 7.5% and 8.5% – the index’s average YTW range for the past year or so.4

We believe that active management and prudent fundamental analysis are critical to identify companies that are well positioned to pay coupons on a timely basis and pay back, or refinance, principal.

Over the long term, the high yield asset class has proven its ability to outperform other parts of the fixed income market. This is principally due to the attractive carry component that compounds through time.

- U291cmNlOiBBWEEgSU0sIEJsb29tYmVyZyBhcyBvZiAyNXRoIEp1bmUgMjAyNA==

- U291cmNlOiBBWEEgSU0sIEJsb29tYmVyZyBhcyBvZiAyNXRoIEp1bmUgMjAyNA==

- U291cmNlOiBBWEEgSW52ZXN0bWVudCBNYW5hZ2Vycy4gSW5kZXg6IElDRSBCb2ZBIFVTIEhpZ2ggWWllbGQgSW5kZXguIFBhc3QgcGVyZm9ybWFuY2UgaXMgbm90IGluZGljYXRpdmUgb2YgZnV0dXJlIHJlc3VsdHMu

High yield also has the potential to compete with equities from a return perspective, but with less volatility.

Since the financial crisis 15 years ago, the high yield asset class has matured significantly in terms of the quality and diversity of companies that make up the market. Many of these companies are household names and global leaders in their lines of business, that feel very comfortable using the high yield market to access capital.

Due to these characteristics and developments, high yield has become much more of a core part of investors’ portfolios, attracting a wide range of investors across institutional, wholesale and retail segments.

As well as the high income available relative to other asset classes, investors are also attracted by the diversification qualities that high yield can offer within a balanced portfolio. With a risk/return profile that sits somewhere between the fixed income and equity markets, high yield can be used in a variety of different ways to suit different investor risk appetites and outlooks.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.