Trump 2.0: déjà vu? Why investors should consider hedging inflation risk

- 19 November 2024 (5 min read)

KEY POINTS

Back in 2016, there were massive fears of global recession as oil prices dropped and China was believed to be slowing down. Then by year end, with Donald Trump’s election, market sentiment shifted and rates sold off by almost 100 basis points (‘bp’) in less than two months. This might sound familiar but there is a key difference today.

What’s different this time?

The themes that drove market sentiment for Trump 1.0 are virtually the same for his second mandate:

- Trade wars: A 10% flat tariff on imported goods (and 60% of those coming from China) will mechanically increase imported goods prices that have been one of the major sources of disinflation this year. The experience of the first mandate shows that tariffs were passed on to consumer prices by almost the exact amount, if that holds true again we could expect a rise in US inflation of 0.5%-1%. These tariffs may be considered as a consumption tax, dampening demand as they are implemented.

- Job market: Based on campaign promises, deportation of undocumented migrants in the US could be as high as eight million, providing a real supply shock to the economy. Some economist studies argue that such scale of labor market contraction could add 3.5% of inflation with a sharp GDP contraction until 20281 . We doubt President Trump will be able to deliver 100% on this promise, but the estimation gives a clear view of the likely consequences of this measure.

- Fiscal Spending: With no surprises, the TCJA extension and further exonerations to public pension funds would increase the public deficit by 1%-2% from 6% currently. This is expected to support growth and would boost inflation in the US through the ‘demand channel’.

However, one thing is different from 2016: the Federal Reserve’s (‘Fed’) starting point on the cutting cycle.

As opposed to the first mandate, the starting point of the Fed Funds rates is different. FOMC members (and we concur) agree on the fact that rates are in restrictive territory. Trump policies are inflationary but at the same time are expected to harm growth as there are no stark productivity gains that would lift the neutral rate of the US economy.

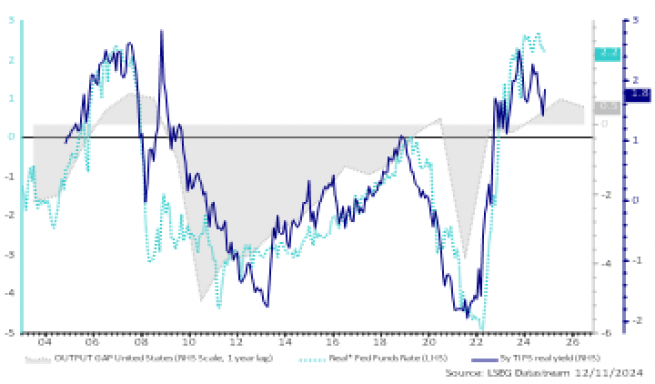

The graph below illustrates how real rates compare to the output gap of the US economy, suggesting that Fed Funds rate is still well above neutral.

- PGEgaHJlZj0iaHR0cHM6Ly93d3cucGlpZS5jb20vcHVibGljYXRpb25zL3dvcmtpbmctcGFwZXJzLzIwMjQvaW50ZXJuYXRpb25hbC1lY29ub21pYy1pbXBsaWNhdGlvbnMtc2Vjb25kLXRydW1wLXByZXNpZGVuY3kiPlRoZSBpbnRlcm5hdGlvbmFsIGVjb25vbWljIGltcGxpY2F0aW9ucyBvZiBhIHNlY29uZCBUcnVtcCBwcmVzaWRlbmN5PC9hPg==

While inflationary pressures resulting from Trump’s policies could push the Fed to be more cautious in its cutting cycle in 2025, we are not expecting rate hikes. Conversely, we see the risk of a marked slowdown in growth that would make the Fed resume more aggressive cuts.

One final consideration is the impact in other economies, like the Euro Area. The weighted average of US tariffs on EU exports is currently around 3%. If we assume an increase to 10%, we estimate it would reduce total Eurozone goods exports by €30bn (0.2% of GDP) and the possibility of higher inflation in the region if retaliation measures are taken.

How to position?

For now, and barring any material spike in productivity, Trump policy intentions appear to be inflationary in the short term and negative for growth (locally and globally) in the medium term. We expect this type of ‘stagflation’ environment to be supportive for inflation-linked bonds.

The 2016 experience confirmed that the inflation-linked bond market does not efficiently forecast inflation but would follow it instead. While inflation breakevens have corrected from the lows seen last summer, we believe that they are still mispricing risks to the upside on future inflation.

Indeed, they are trading at levels consistent with the 2% objective so there is little inflation premium priced into current valuations. We are tactically long US breakevens as we expect them to move higher, as the inflation premium builds in valuations. Inflation-linked bonds have continued to outperform their nominal counterparts and we expect them to continue to do so given the current environment.

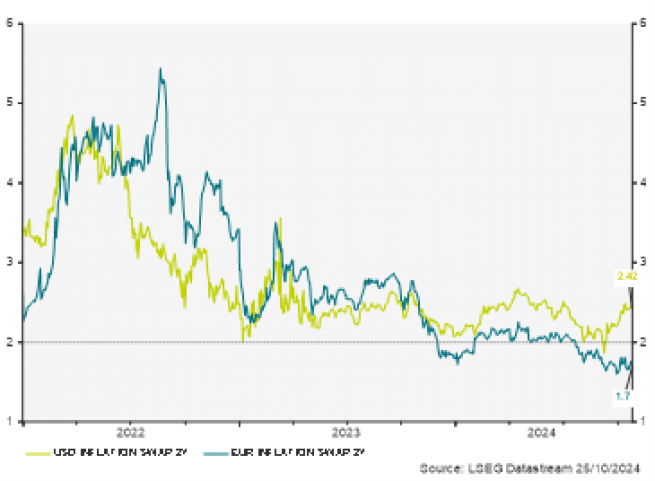

The graph below shows 2 years inflation swaps slightly above the 2% target for the Federal Reserve and well below for the Euro Area.

Making short-dated linkers great again

On a more structural basis, we prefer to be invested in the shortest maturities on the inflation linked bond curve that are more likely to track realised inflation. They are not only less volatile, but they could benefit from higher levels of indexation if inflation reaccelerates, while having less duration risk.

Also, the current level of real yields is not consistent with potential growth, and this is particularly acute in the Euro Area and the UK where we expect Central Banks to be more aggressive in their rate cutting cycle.

Inflation is certainly expected to be more uncertain and volatile than in the previous decade. The recent Trump election victory may be another wake-up call for investors to consider hedging the inflation risk of their portfolios and to consider linkers in their core asset allocation.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.