Eurozone Outlook – Slowly taking off

- 04 December 2024 (5 min read)

Modest growth acceleration with downside risks

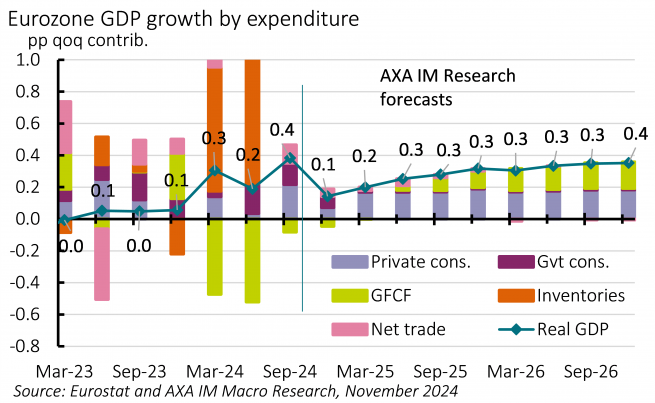

We expect the Eurozone’s protracted economic rebound to continue and given Q3’s stronger-than-expected performance we have revised our 2024 growth forecast up to 0.8% (up 0.1 percentage points). But beyond this, we maintain our below-consensus stance, projecting GDP growth at 1.0% in 2025 and 1.3% in 2026 (Bloomberg consensus: 1.2% and 1.4%). Our outlook is unchanged, anticipating expansion to recover slowly, led by private consumption in 2025, while investment should eventually make a firmer contribution in 2026.

Negotiated wage growth has exceeded inflation since Q3 2023, implying real purchasing power gains. However, the household saving rate has also been trending higher, culminating at 15.7% in Q2 2024, and acting as a brake to private consumption growth. Although we expect real wage growth to decelerate, we also anticipate some normalisation of the saving rate, implying a moderate but persistent pickup in consumer spending (Exhibit 7). However, the unprecedented recent savings behaviour makes it inherently difficult to forecast the timing and magnitude of such an acceleration.

We anticipate that investment will gently restart from the second half of 2025, following a year of progressive relaxation of monetary policy restrictiveness – and likely outright monetary easing to come – more than offsetting a reduced drag from profit margins.

Risks to our Eurozone growth forecasts are skewed to the downside. Trade policy and geopolitical uncertainty are running high after the US elections outcome. These come at a time when European political decisiveness is in question with several countries run by fragile coalitions. Notably, Germany is set to hold a general election on 23 February 2025, while snap elections in France and Spain cannot be ruled out. Increased political and economic uncertainty may imply that persistent manufacturing woes could spill over to services, leading to a quicker and more meaningful correction in the unemployment rate, projected to average 6.6% and 6.8% in 2025 and 2026 after 6.4% in 2024.

Inflation to stabilise below ECB’s target

Headline inflation markedly eased in 2024 and should average 2.3%, down from 5.5% in 2023. We see a continued shift from better supply conditions to weaker demand continuing to affect price dynamics. Due to this weak domestic demand outlook, we project inflation to stabilise at 1.9% in 2025 and 1.7% in 2026, below the European Central Bank’s (ECB) 2% target.

Eurozone core inflation should continue to edge down, to 2.1% in 2025 and 1.9% in 2026, from 2.8% this year. Though decelerating, we see services prices remaining the main inflation driver. By contrast, we foresee a pick-up of goods inflation pushing higher to 1.1% in 2025 and 1.3% in 2026 from 0.9% this year. We also expect food inflation to stabilise at its current level of around 3%, while the contribution from energy is expected to be slightly negative as market price futures continue to point to a weaker outlook. Such dynamics are likely to be only partially offset by the further expiry of energy crisis government support measures.

Towards an accommodative monetary policy stance

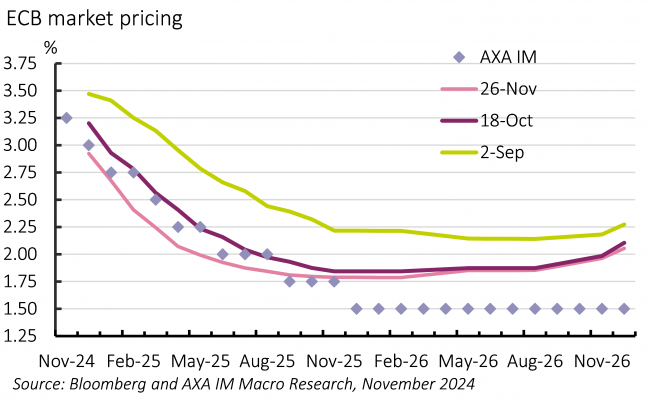

Our Eurozone sequential 2025 growth forecast (0.27% quarter-on-quarter on average) remains below estimates of potential growth (0.33%). Coupled with an undershoot of the ECB’s inflation target for most of 2025, there is an obvious case for a continued unwinding of the central bank’s restrictive stance. We continue to expect back-to-back 25-basis-point deposit rate cuts to reach 2.0% by next June, close to the vicinity of neutral rate territory.

Our projected path for 2026 sees a modest acceleration to potential growth, consistent with a continued undershooting of inflation (1.7%). This should push the ECB towards an accommodative policy stance. We expect it will cut twice in the second half of 2025, bringing the deposit rate to 1.5%, below current market pricing (Exhibit 8). Given the downside risks to growth, we think this could come sooner than end-2025, with the ECB forced into more accommodative territory.

There are two reasons that are likely to make the ECB more proactive in its policy response. First, compared with past years, weak Eurozone growth has rebalanced from supply to demand factors, on which the ECB can have more bearing via changes in its interest rate policy. Second, during the move towards a more accommodative stance, ECB risk management may encourage aggressive action to avoid being eventually pushed into extra-ordinary measures, including negative interest rates and/or quantitative easing.

Despite minor funding pressures arising, we do not think that the ECB is likely to alter the pace of balance sheet reduction, with excess liquidity projected to land at around €2.5tn by end-2026, still well above pre-pandemic levels. That said, we will watch for further details on the long-term aspects of the ECB’s operational review, including prospects for long-term liquidity injections and structural bond portfolios.

Fiscal policy: France to remain in the spotlight

The Eurozone’s stretched public finances will remain in focus across the bloc. However, for the first time in four years, countries have submitted budget plans following the application of (revised) EU rules after four years of suspension.

Nevertheless, we doubt the Eurozone’s fiscal stance will be as restrictive as suggested in these plans – Germany’s general election should offer an example of this. Moreover, several member states’ budgets have been built on optimistic growth assumptions, likely leading to slippage versus targets, notably France – the European Commission’s autumn forecasts concur. Finally, Italy and Spain are scheduled to receive increased amounts of Recovery and Resilience Facility funds next year.

Furthermore, France and Italy’s public debt-to-GDP ratios are rising due to delayed deficit reduction, reflecting a challenging planned adjustment for the former while still accounting for the ‘superbonus’ tax credit for the latter. This highlights the vulnerability of these two countries – and the Eurozone as a whole – in case these downside risks to growth materialise.

Politics: No momentum to address key issues

German Chancellor Olaf Scholz ended the country’s traffic-light coalition, calling for a snap election on 23 February 2025 – nine months ahead of schedule. Current polls show a likely CDU/CSU and SPD coalition return, although it is uncertain whether they will have enough votes to muster an outright majority in Parliament. It is not our base case scenario that Germany’s fiscal stance turns accommodative – a two-thirds Parliamentary majority required to overturn the debt brake rule looks prohibitive – rather, we envisage a slightly less restrictive stance. In sum, these elections are unlikely to prove a game changer for domestic, nor European, prospects.

Fragile government coalitions also exist in France and Spain; such that we cannot rule out snap elections in either over the next couple of years. These developments also emphasise the weakness to the new European Commission.

This puts Europe in a weak political and policy position when facing the renewed economic challenges, it’s likely to encounter from a new Donald Trump US presidency. Tariff hikes, domestic or global, could add to longstanding economic challenges including demographics, competitiveness and low productivity growth. Weak governments in key capitals could also increase the challenge of effective responses to arising geopolitical issues, of which Ukraine may be uppermost for Europe, but may also include the Middle East and climate change challenges.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.