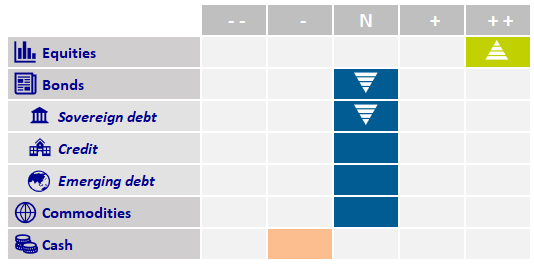

Multi-Asset Investments Views: Riders on the storm

- 28 March 2025 (7 min read)

KEY POINTS

Pessimism and uncertainty characterised the past month for many investors, when the real-time Atlanta Federal Reserve US GDP growth tracker fell precipitously into negative territory, to -2.8% on an annualised basis. But to analogize The Doors, our fundamental analysis points to more Strange Days, rather than This is the End.

US retail sales came in much softer than expected for January - a combination of extreme weather (with some shops temporarily closing rather than facing the wrath of nature) and some pullback after strong December spending. Add to this net trade statistics, which were upended by record-high gold imports, and sprinkle some policy uncertainty over tariffs on top - and the market had the perfect recipe of a US growth scare.

Our Macroeconomic Research team has downgraded its US GDP growth forecast for the first quarter (Q1) of this year (to barely positive) and consequently lower for the full year. Yet it’s not all doom and gloom due to the nature of the one-off shocks and we continue to expect an upside boost to growth in Q2 as activity reverts to more normal spending levels. Most importantly, we do not expect a US recession in the next few quarters with growth hovering around 2% annualised, private job creations still around 100,000 per month and hence any rise in US unemployment to be marginal.

Our prudent fundamental optimism stems from the main US growth engine: its resilient consumer. After years of strong spending, some slowdown in private consumption seems reasonable, as the savings surplus accumulated during COVID-19 has been fully unwound. US households’ saving ratio is now down to an historically low level, leaving little to no additional support to consumption beyond real income growth.

Typical of the late stage of the economic cycle that we are in today, we are seeing a rise in US credit card loans delinquency rates, which now stands above 3%, a 13-year high1 . This might seem alarming but the past 13 years have seen abnormally low levels, as the pandemic and the unprecedented economic policies that followed artificially collapsed this delinquency rate from its slow cyclical rise in late 2019 and early 2020. Ahead of previous US recessions (such as mid-1990 or late 2007), even mild ones (like early 2001), the delinquency rate was much higher than current levels, north of 4.5%. The same pattern can be found in consumer loans. If anything, the latest data show a modest improvement with delinquency rates coming down in the second half of 2024 – which is in line with the easing of financial conditions (long-term interest rates down, US dollar down and credit volumes up).

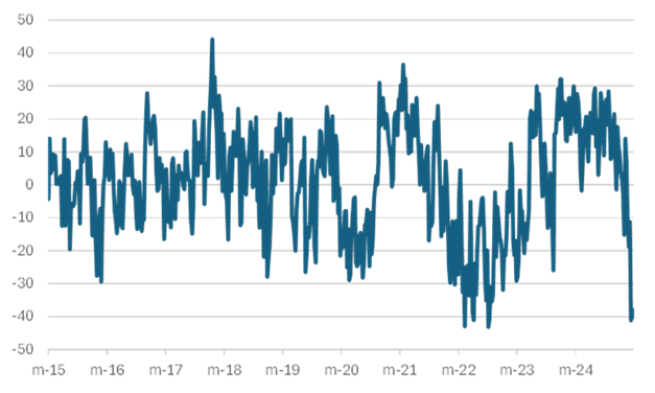

Our decision to tactically increase exposure to US equities is driven primarily by extremely depressed sentiment and positioning, rather than by macroeconomic fundamentals. As the chart shows, the share of individual US investors now expressing a bearish view is at one of its highest levels ever, which coincided in previous instances with a short-term stock market rebound. Once pessimism becomes widespread, some investors are likely to adopt a more constructive way of thinking, meaning sentiment could shift to become neutral or even outright optimistic. Positioning data from speculative investors, as well as systematic strategies, also point to historically depressed exposure, usually associated with a contrarian buy signal. Recent retail investor flows appear to support this contrarian view.

- U291cmNlOiBGZWRlcmFsIFJlc2VydmUgQmFuayBvZiBTdCBMb3VpcywgMTggTWFyY2ggMjAyNQ==

The start of 2025 saw rare US equity market underperformance relative to the rest of the world, and European equities significantly outperforming. This surge in was in part attributed to some fundamental macroeconomic improvements but also to positioning: the recent US technology and growth stocks focus had left global investors markedly underexposed to European stock markets. This positioning has rapidly inverted and is now even starting to look over-extended, putting this stellar overperformance at risk of profit taking. Overall, we stick to favouring the US within our equity allocation, along with China, which is now experiencing a domestic-driven revival, while also benefiting from a valuation catch-up in technology companies relative to their US counterparts.

Turning to fixed income, Eurozone bonds yields rose sharply, as promises of large public investments into infrastructure and defence both from Germany and the wider bloc were factored into higher GDP growth expectations. Term premiums – the return investors expect for holding longer-term rather than shorter-term bonds – also rose, given the expected heavier future debt issuance.

Our Macroeconomic Research team forecasts GDP growth of just 0.8% for the Eurozone this year, a view recently matched by consensus estimates. We therefore remain sceptical that the sell-off in euro-denominated bonds has much further to go. Overall, we maintain the interest-rate sensitivity of our portfolios in line with their respective long-term targets and continue to expect some recovery in the weeks ahead.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved

Image source: Getty Images