How investors can get on board with sustainable travel and transport

- 13 June 2023 (7 min read)

Key points:

- International travel is returning to near pre-pandemic levels, highlighting the sustainability challenges for the sector

- Policymakers are taking decisive action to reduce emissions from transport while new technologies are popularising alternative methods of travel, and helping decarbonise existing ones

- The combination of new policies and technological innovation is creating a wave of long-term investment opportunities

International tourism is expected to return to almost pre-pandemic levels this year,1 but this poses something of a conundrum. How do we combine the economic and wider benefits of travel with the increasing urgency of the need to tackle climate change?

The answer, quite clearly, is decarbonising methods of transport and travel – but while the answer is simple, the process of getting there is not. However, this journey towards lower carbon travel is underway, and creating potential new opportunities for investors now and in the future.

From electric vehicles and sustainable aviation fuels to micro-scooters, we have seen a wave of innovation in the transportation sector over recent years, with new technologies popularising alternative methods of travel, and helping decarbonise existing ones.

Governments and policymakers are also taking drastic action in a bid to reduce emissions – France has banned short-haul flights where train alternatives exist,2 while the Netherlands has limited the number of flights at Schiphol airport, a key travel hub.3

But governments don’t want to put the brakes on international travel and tourism – a sector that contributed 7.6% to global GDP last year and created 22 million new jobs.4

For many countries, attracting hordes of foreign tourists is vital to their economy.

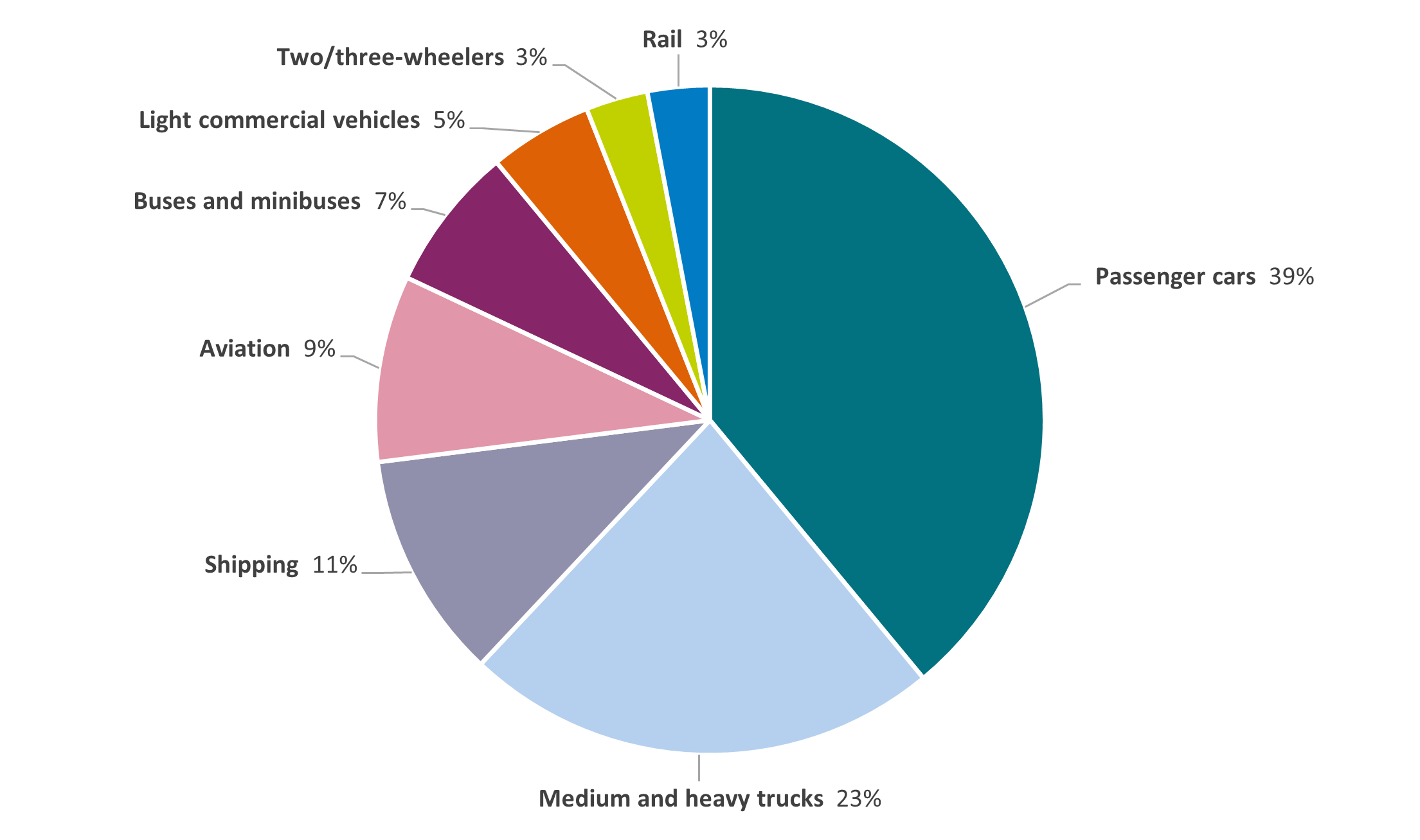

However, travel and tourism accounts for between 8% and 11% of total global carbon emissions, according to varying estimates – which is almost certain to increase as travel activity is predicted to surge by 85% from 2016 to 2030.5 Passenger cars are the largest contributor to transport sector carbon emissions, at 39%, followed by medium and heavy trucks (23%) and shipping (11%). Rail travel accounts for just 3% of emissions.6

Carbon emissions from transport by sub-sector

Source: Statista, based on 2021 data

Low-carbon fuels

Mile for mile, flying is the most carbon-intensive method of travel – the aviation industry is thought to be responsible for around 5% of global warming.7 It is therefore a key sector where investors can look to direct capital towards companies driving progress. Decarbonising air travel is highly complex, but experts are looking at everything from fuel and manufacturing to aircraft and airport design.8

Many airlines have already made commitments to using sustainable aviation fuel (SAF). A biofuel with similar chemical properties to conventional aviation fuel, SAFs have potentially sharply lower greenhouse gas emissions – but are currently expensive and hard to come by.

This may change in future as the US Inflation Reduction Act includes subsidies for SAF production while the European Union is reported to be considering setting SAF usage targets from 2030 for any airline seeking to receive a green label.9

Changing consumer preferences can also help shift the dial – a recent survey found that 40% of travellers were willing to pay at least 2% more for carbon-neutral flights.10 Another solution could involve decentralising travel hubs. For example, moving from central to regional airports helps boost local economies, bringing tourism as well as jobs to those areas, and reduces some of the strain on capital cities, which can be heavily congested with traffic and suffer from higher levels of pollution including noise.

Meanwhile the cruise industry is the fastest growing tourism sector and is expected to exceed pre-pandemic levels in passenger numbers and revenues by 2026.11 Cruise ships are carbon-intensive, but the industry is investing in new technologies and reducing emissions.12 Royal Caribbean is aiming to launch a zero emissions ship by 2035,13 while at the other end of the scale the Thames Clipper, the London river bus service, is going hybrid.14

Electric vehicles on the rise

Cars are the biggest contributor overall to transport sector emissions, at some 39%, in part due to the sheer number of vehicles on the road.15 Governments around the world are putting in place new policies and targets to reduce emissions, such as banning the sale of new petrol and diesel cars in the Eurozone and UK in the coming years,16 while India aims for all two and three-wheeled vehicles, including auto-rickshaws, to be electric by 2025.17

Sales of electric vehicles (EVs) are expected to rise 35% this year,18 and as well as the EV manufacturers themselves, such as Tesla, there is scope to invest in companies that make batteries, parts and charging infrastructure for electric vehicles and more.

Reducing the number of cars on the roads is also another step towards lower carbon emissions. Ridesharing potentially reduces the need for car ownership, particularly in cities, and opens up a new swathe of companies for investors to consider - but a recent study suggests it is pricing that makes the difference between whether ride sharing reduces or increases emissions.19

Rail travel has one of the smallest carbon footprints of transport methods,20 but passengers remain at the mercy of timetables and set routes. However, companies in this sector are harnessing technology to improve their services and appeal more to customers – for example using e-tickets to reduce paper waste and making emissions data more accessible to allow them to understand the carbon impact of their journey.21

And while artificial intelligence has had mixed press recently, there’s no doubt it can be helpful in certain areas – in transport for instance, companies are using artificial intelligence and cloud computing to deliver smarter timetables to meet changing customer demand.22

Meanwhile electric trains and trams harnessing new technologies including automation can provide low carbon alternatives in cities and new urban developments. The global connected rail market is already estimated to be worth over $92bn and to reach over $143bn by 2030.23

At the smaller end of the scale, we are seeing a surge in popularity of micro-mobility – electric bikes and scooters. The COVID-19 pandemic caused a spike in demand for these kinds of powered two-wheelers as an alternative to public transport.24

Micro-mobility now accounts for an estimated 16% of trips globally, according to McKinsey & Company. It estimates that the market is worth around $180bn today, with the potential to more than double by 2030 to around $440bn.25 From e-bike manufacturers like Yamaha and Taiwan’s Giant Bicycles, to Bosch, a company perhaps better known for appliances like washing machines – but which also makes motors and rechargeable batteries for electric bikes – there are a myriad of prospective opportunities for investors to consider as the sector evolves.

Driving potential investment opportunities

The economic downturn and high inflation are likely to mean consumers are more demanding when it comes to spending their money on leisure travel – and they are increasingly aware of the environmental impact and becoming more selective about sustainability issues when travelling.26

There is ongoing impetus from governments and policymakers, which we expect to only increase as they strive to meet climate targets, both in encouraging lower carbon forms of travel and granting incentives for investment in decarbonisation.

Companies everywhere are setting sustainability targets, many including emissions from business travel, which represents nearly a third of all travel spend.27 We believe that those which are at the forefront of the transition to sustainable travel, whether directly or indirectly – such as via the infrastructure needed - are likely to benefit from increased customer demand.

As the market continues to return to, and likely exceed, pre-pandemic levels, we see scope for potential investment opportunities for those who want to play a part in the journey to sustainable travel while also seeking financial returns.

- QmFyb21ldGVyIHwgVU5XVE8=

- RnJhbmNlIGJhbnMgc2hvcnQtaGF1bCBmbGlnaHRzIHRvIGN1dCBjYXJib24gZW1pc3Npb25zIC0gQkJDIE5ld3M=

- U2NoaXBob2wgYWlycG9ydCBpbiBBbXN0ZXJkYW0gbGltaXRzIGZsaWdodHMgdG8gcHJldmVudCBlbWlzc2lvbnMsIGluIHdvcmxkIGZpcnN0IHwgRXVyb25ld3M=

- VHJhdmVsICZhbXA7IFRvdXJpc20gRWNvbm9taWMgSW1wYWN0IHwgV29ybGQgVHJhdmVsICZhbXA7IFRvdXJpc20gQ291bmNpbCAoV1RUQyk=

- QWNjZWxlcmF0aW5nIHRoZSB0cmFuc2l0aW9uIHRvIG5ldC16ZXJvIHRyYXZlbCB8IE1jS2luc2V5

- R2xvYmFsIHRyYW5zcG9ydCBDTzIgZW1pc3Npb25zIGJyZWFrZG93biAyMDIxIHwgU3RhdGlzdGE=

- U2hvdWxkIHdlIGdpdmUgdXAgZmx5aW5nIGZvciB0aGUgc2FrZSBvZiB0aGUgY2xpbWF0ZT8gLSBCQkMgRnV0dXJl

- VGhlIGZ1dHVyZSBvZiBmbHlpbmcgKGNhbS5hYy51ayk=

- RVNHIFdhdGNoOiBEZXNwaXRlIHNldGJhY2tzLCBncmVlbiBmaW5hbmNlIGVuZHMgMjAyMiBpbiBnb29kIGhlYWx0aCB8IFJldXRlcnMgLyBFVSBQbGFucyB0byBHaXZlIFBhcnRzIG9mIEF2aWF0aW9uIEluZHVzdHJ5IGEgR3JlZW4gTGFiZWwgLSBCbG9vbWJlcmc=

- QWNjZWxlcmF0aW5nIHRoZSB0cmFuc2l0aW9uIHRvIG5ldC16ZXJvIHRyYXZlbCB8IE1jS2luc2V5

- Q3J1aXNlIGluZHVzdHJ5IGZhY2VzIGNob3BweSBzZWFzIGFzIGl0IHRyaWVzIHRvIGNsZWFuIHVwIGl0cyBhY3Qgb24gY2xpbWF0ZSB8IFJldXRlcnM=

- MjAyMyBTdGF0ZSBvZiB0aGUgQ3J1aXNlIEluZHVzdHJ5IFJlcG9ydCB8IENsaWE=

- MjAyMSBFbnZpcm9ubWVudGFsLCBTb2NpYWwgYW5kIEdvdmVybmFuY2UgUmVwb3J0IHwgUm95YWwgQ2FyaWJiZWFuIEdyb3Vw

- SHlicmlkIGJvYXRzIHRvIHJldm9sdXRpb25pc2Ugc3VzdGFpbmFibGUgcml2ZXIgdHJhdmVsICh0aGFtZXNjbGlwcGVycy5jb20p

- R2xvYmFsIHRyYW5zcG9ydCBDTzIgZW1pc3Npb25zIGJyZWFrZG93biAyMDIxIHwgU3RhdGlzdGE=

- RVUgYmFuIG9uIHNhbGUgb2YgbmV3IHBldHJvbCBhbmQgZGllc2VsIGNhcnMgZnJvbSAyMDM1IGV4cGxhaW5lZCB8IE5ld3MgfCBFdXJvcGVhbiBQYXJsaWFtZW50IChldXJvcGEuZXUpIC8gVGhlIFRlbiBQb2ludCBQbGFuIGZvciBhIEdyZWVuIEluZHVzdHJpYWwgUmV2b2x1dGlvbiAoSFRNTCB2ZXJzaW9uKSAtIEdPVi5VSyAod3d3Lmdvdi51ayk=

- SW5kaWEgdHVybnMgdG8gZWxlY3RyaWMgdmVoaWNsZXMgdG8gYmVhdCBwb2xsdXRpb24gLSBCQkMgTmV3cw==

- RGVtYW5kIGZvciBlbGVjdHJpYyBjYXJzIGlzIGJvb21pbmcsIHdpdGggc2FsZXMgZXhwZWN0ZWQgdG8gbGVhcCAzNSUgdGhpcyB5ZWFyIGFmdGVyIGEgcmVjb3JkLWJyZWFraW5nIDIwMjIgLSBOZXdzIC0gSUVB

- RW5lcmd5IGFuZCBlbnZpcm9ubWVudGFsIGltcGFjdHMgb2Ygc2hhcmVkIGF1dG9ub21vdXMgdmVoaWNsZXMgdW5kZXIgZGlmZmVyZW50IHByaWNpbmcgc3RyYXRlZ2llcyB8IG5waiBVcmJhbiBTdXN0YWluYWJpbGl0eSAobmF0dXJlLmNvbSk=

- V2hpY2ggZm9ybSBvZiB0cmFuc3BvcnQgaGFzIHRoZSBzbWFsbGVzdCBjYXJib24gZm9vdHByaW50PyAtIE91ciBXb3JsZCBpbiBEYXRh

- RW52aXJvbm1lbnRhbCBTdXN0YWluYWJpbGl0eSB8IFRyYWlubGluZSBwbGMgKExTRTogVFJOKSAodHJhaW5saW5lZ3JvdXAuY29tKQ==

- R3JlZW5lciBTbWFydGVyIHRyYXZlbCAtIFN0YWdlY29hY2ggR3JvdXA=

- R2xvYmFsIENvbm5lY3RlZCBSYWlsIE1hcmtldCBTaXplIFJlcG9ydCwgMjAyMiAtIDIwMzAgKHBvbGFyaXNtYXJrZXRyZXNlYXJjaC5jb20p

- U2FsZXMgb2YgZWxlY3RyaWMgYmljeWNsZXMgYXJlIHVwIGFsbCBvdmVyIHRoZSB3b3JsZCB8IFdvcmxkIEVjb25vbWljIEZvcnVtICh3ZWZvcnVtLm9yZyk=

- VGhlIGZ1dHVyZSBvZiBtb2JpbGl0eSBpbiAyMDM1IHwgTWNLaW5zZXk=

- VHJhdmVsIFN1c3RhaW5hYmxlIHwgU3VzdGFpbmFiaWxpdHkgYXQgQm9va2luZy5jb20=

- QWNjZWxlcmF0aW5nIHRoZSB0cmFuc2l0aW9uIHRvIG5ldC16ZXJvIHRyYXZlbCB8IE1jS2luc2V5

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2023 AXA Investment Managers. All rights reserved